EZV Algorithms, Jul-23-2025: A New Yield Symbol To Ponder, BTCC

I’ve been trading bitcoin ETFs for most of a year now; IBIT is my ETF of choice because it reflects spot bitcoin values and option liquidity facilitates hedges when I want to cut risk. GBTC would work equally well. Bitcoin (BTC) is volatile and so are the spot ETFs; bitcoin’s worst drawdown predates the inception of ETFs, but it was 83% in 2018 which is intolerable. It spent most of 2018 in the sewer, so recovery was a relative slog. So the algorithms are very risk-averse even if it means foregoing some gains for a period.

The flipside of that observed volatility is the ability to capture the time value in options associated with elevated implied volatility. GBTC, for example, shows 7-day ATM calls with a time value of $2.17 on a $93 ETF price. That’s 2.33% over 7 days from a covered call as long as GBTC rises or stays the same. Compound that over a 252-day year to get a 129% return, but only in a consistently rising BTC market. Ignore compounding and it still means a potential yield of 83% . It’s difficult to guess at realistic returns because when BTC drops IVs rise, and so do opportunities; give a little back and make more on the next cycle. My personal guess is that a 40% to 60% yield is possible but with some risk. Of course the algorithm could help with risk.

So, this past week I discovered BTCC with a very recent April-2025 inception date; it makes a business of selling calls on GBTC, covered and otherwise. Its last reported composition shows 27% in near cash with the remaining holdings in covered calls or collateral-supported short calls. The structure provides some diversification of risk. Cash is a buffer, and covered calls are exposed to an underlying BTC decline while the collateralized calls are subject to a unusual BTC rise. It looks to me that the composition’s design weights those risks more heavily toward upside exposures but less heavily to the greater-magnitude downside risk. I like that.

Clearly risk is mitigated by professional management, but given the short history and inadequate composition detail, any precise risk assessment would be a guess, except to say it is less than a straight covered-call strategy.

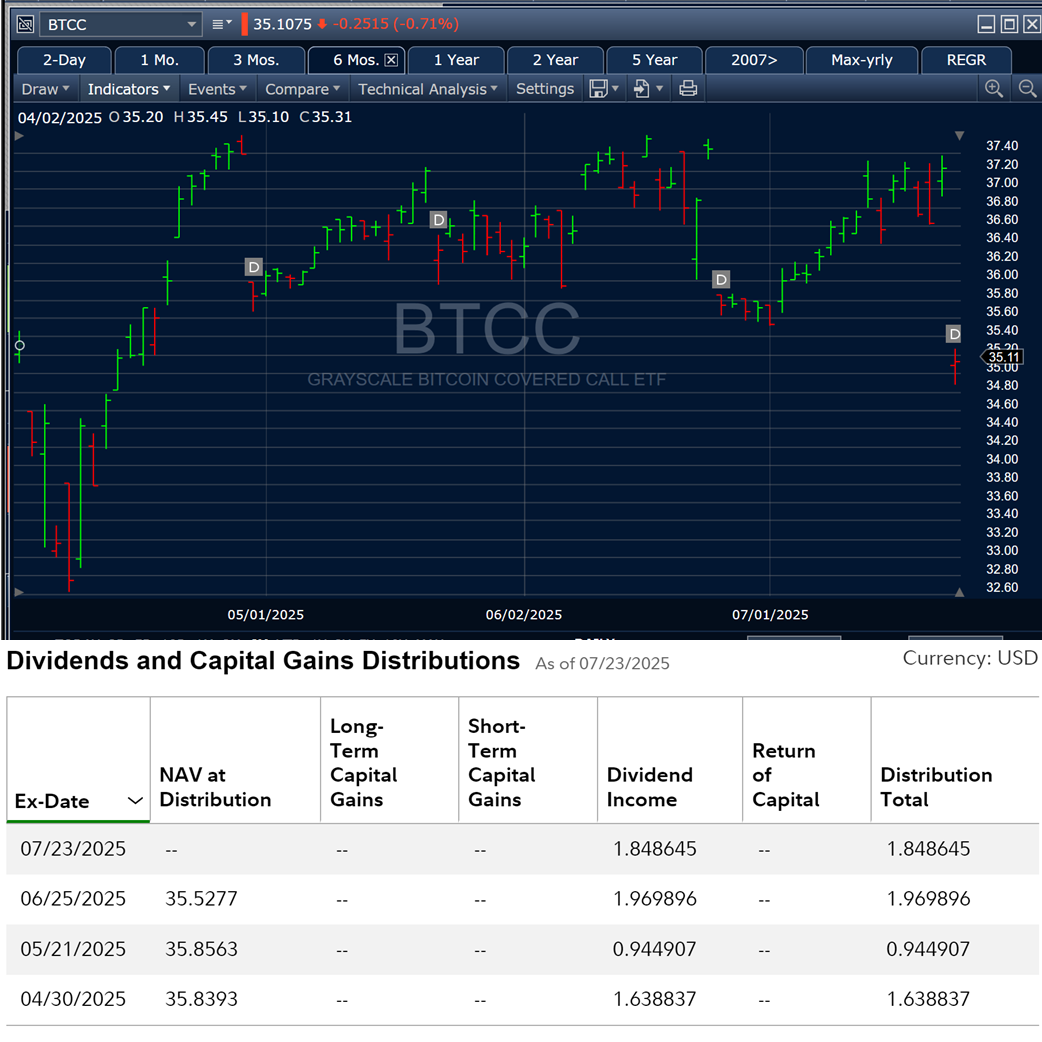

Let’s look at BTCC’s short history of price and dividends. This is taken from Fidelity and those periodic drops are just ex-dividend dates.

BTCC trades at about $36 and it’s paid $6.40 in the last 4 months. Annualize that at twelve-fourths and it equates to a $19.20 annual rate. That would be a 71% dividend rate, consistent with the numbers compiled above for GBTC time-value capture. Keep in mind that GBTC has been rising since April. Superficially that might sound like a low-risk environment, but given the skewed composition, I’m not so sure.

Here is my takeaway. BTCC seems to be an undiscovered gem. If the short history of dividends is remotely sustainable, it offers great yield potential. And if the yield is sustainable, imagine what the capital appreciation might be. I bought a chunk today on its ex-dividend drop.

Surely you can find someone to share this with. — Mike G

Mike- regarding your point: “My personal guess is that a 40% to 60% yield is possible but with some risk. Of course the algorithm could help with risk.”

How can algo help with covered call strategy? I understand that I can use algo to buy and sell on signal but how do I leverage it to improve results of covered calls?